r/HealthInsurance • u/quinndoline • 28d ago

Plan Choice Suggestions Starting a new job and these are my coverage options. Kind of freaking out

{kind=link}

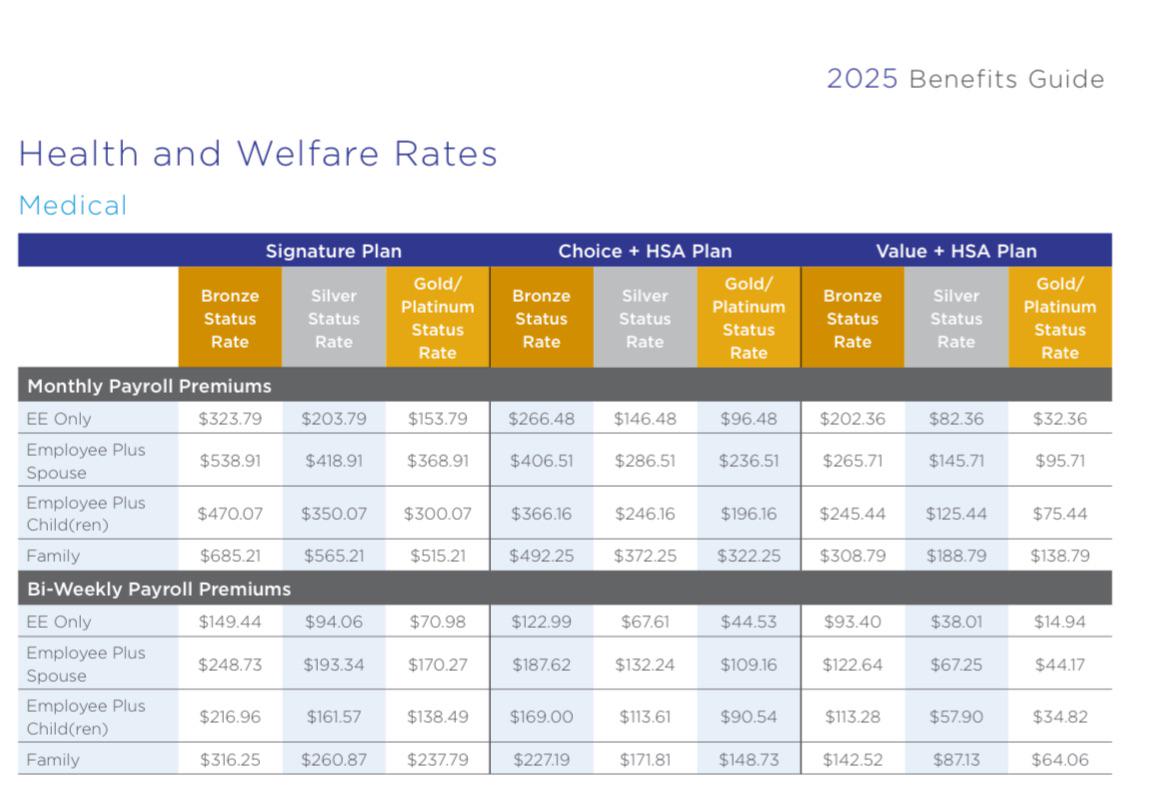

Starting a new job in about 2 weeks, and these are the options for coverage. My old job had Aetna, and I paid about $100 a month for the highest coverage, lowest deductible plan. Granted my company only offered us two options, but my premium was less than $100 with a non-smoking credit and my deductible was only $800. Now I am switching to a new position in the field I want to work in, but the new insurance (United) seems to leave a lot to be desired. The different “tiers” come from a separate app called Vitality where you earn points for various random things like app health screenings, getting check ups, and doing “goals check ins”. From the looks of it, it will take several months to a year to earn the amount of points to get to silver tier even when maxing out points, and even if I get there it is not clear whether the upgrade is automatic or whether I have to wait for the following year. It all just feels very convoluted and as someone in a not very high paying field (publishing) the $200 premium for the most bare bones, high deductible coverage is scaring me. The deductibles for the different plans (starting from lowest premium to highest, reading from right to left on chart) are $3300, $1650, and $500 respectively. I have 3 regular prescriptions I can’t go without, and I see an audiologist/otologist a few times a year for check ups after hearing restoration surgeries I had this year and last year. Would love to hear other people’s experiences with this kind of structure and any advice on what plan seems best for someone making less than $50k yearly.

32

u/Illustrious-Jacket68 28d ago

I don’t know if this makes you feel better but I have to pay more for worse coverage. It will vary from company to company because of what they negotiate and the size/volume of what they can provide. Crazy times we live in….

One thing to also look at is whether your medications actually are cheap/cheaper going through other means - e.g. amazon pharmacy, goodRX, etc. I found that the price of them is pretty low - almost as low as my current copay.

20

u/LizzieMac123 Moderator 28d ago

So it sounds like the more wellness you complete, the lower your premiums are. This is pretty perfectly acceptable to essentially gives wellness credits- a reward for getting your preventive care done and having a healthy lifestyle.

As far as when the next tier kicks in, thats a question for your HR- i typically see them on an annual basis- as in if you did the wellness in 2025, youd get the wellness credit for 2026's benefits- but yours may change mid-year.

To be fair, an employer with 50 employees or more only has to offer 1 plan that is no more than 9.02% of your income. At 50k income, that works out to about 375$ per month- so ALL of these meet affordability standards, even at the bronze levels.

Just a hint- once youre offered a job at a new place, always ask for the benefits details so you can get a full scope of your total compensation. Benefits can vary a lot from employer to employer.

We also have a pinned post on how to pick a plan. Give that a read and ask your specific questions here.

2

u/LadyGreyIcedTea 27d ago

Just a hint- once youre offered a job at a new place, always ask for the benefits details so you can get a full scope of your total compensation. Benefits can vary a lot from employer to employer.

Absolutely this. You should never accept a job without having seen/evaluated the benefits. I am currently trying to negotiate salary because the health insurance at the company that just offered me a job is significantly worse than what I have now and I'm not switching from no deductible to a $5K family deductible unless they make the offer very worth my while.

I hate how health insurance is tied to your job in the US though. More than once I've had to make employment decisions because of health insurance.

1

-1

u/Unlucky-Work3678 28d ago

Interesting that I didn't know there is the 9% rule. But still, 9% is more than SS tax and California 9.1% tax tier (which most people are in).

16

u/Which-Ad-2020 27d ago

Wouldn't it be so much easier if you didn't have to go through this if we just had Universal Healthcare? Having health insurance through your job is such a pain in the ass and a scam.

3

8

6

u/Magentacabinet 28d ago

So the big question is do you want to pay more for the coverage every month or do you want to pay more when you go to the doctor?

If you're paying more for the coverage every month you're paying less when you go to the doctor.

If you're paying less for the coverage every month you're paying more when you go to the doctor.

How often do you go to the doctor?

3

u/RedHeadedStepDevil 27d ago

After being in a position where I couldn’t afford to go to the dr (or for medication, or PT or surgery), my mindset is to buy the best insurance one can afford, with the lowest deductible and lowest out of pocket expenses.

6

4

u/Same-Effective2534 27d ago

Wow, I wish I even had these as options at all. I'm paying $1100 for a shitty bronze plan with a 14k deductible.

1

5

u/miteymiteymite 27d ago

Your old insurance was super super cheap and not common. These new prices look really good.

3

u/Glittering-Ad-7463 27d ago

That is really hard. I know it can be challenging to get benefit info before you accept a new job too, so it is hard to make an educated decision. The old plan you had is much more the rarity. If you would have been able to get this info before accepting, you might have been able to negotiate salary with that in mind. Definitely check to see about being able to be covered under a spouse if you have one. UHC also tends to be very challenging when it comes to denying claims :-(

3

u/AwkwardDuckling87 27d ago

Someone explain to me like I'm a child- why are higher tier platinum plans less expensive than bronze plans?

6

u/UniversityAny755 27d ago

The tiers aren't the plan levels but the employee's "wellness" level. It's a way to incentivise employees to do things like quit smoking, lose weight, get preventive care done, get s yesrly flu shot, etc.

My company does this, and it's a huge cost savings for me and honestly really easy as a generally healthy person with good habits.

5

u/AwkwardDuckling87 27d ago

Thank you! I was so confused as those names are used for many insurance plans to denote coverage tiera.

7

u/loftychicago 28d ago

Your old insurance was dirt cheap. These premiums look reasonable, although having only UHC is unfortunate.

6

u/Intrepid_Bicycle7818 28d ago

Does your husband’s company offer a better plan that makes more sense for you?

You can waive your plan and join his.

4

u/Rootaah22 27d ago

I would kill for those rates. $1700/month family premiums where I work. 0 for me…add wife and kids…boom. I’m planning on pulling my family off employers plan this fall and taking my chances with the ACA. I gotta believe I can get them better cost coverage than the insane costs my company provides.

2

u/Rdbjiy53wsvjo7 27d ago

We went through ACA for Colorado, did not do it based on income because it's highly variable right now, for a family of 4, including medical, dental, and vision, we are paying $1400/month and our deductible for family is around $3000, HSA, Cigna.

Made me realize my previous employer wasn't giving us much of a discount, which really sucks, but I thought it was going to be twice as much.

2

u/quigonskeptic 27d ago

You can check on the ACA now to verify. But typically you're not eligible for any subsidy if you are declining insurance through work.

2

u/curmudgeonlyboomer 27d ago

your employer may also be contributing something toward the hsa which does not appear on this chart.

2

1

u/Capable-Listen3204 27d ago

No need to freaking out about this as the chart is just basic pretty much standard benefit chart. I would choose either tier 2 or tier 3 benefit if you are heavily rely on the prescriptions drug for recovery, as i am at the similar situation as yours. Also, your boss will be the one who responsible to pay most part of the monthly insurance bills dues when you are only responsible only for 10 to 10ish % on your paycheck. Don't choose the options that affect your need.

1

u/marimillenial 27d ago

If it makes your feel better, my job covers my insurance premium completely, but it’s $600 a month to add my child for the cheapest HDHP premium.

1

1

u/Other_Albatross7331 27d ago

Lmao I just came across an old benefits paper from 2013, my family premium was $46 for PPO (weekly). Now it’s $225 week with a 3500 deductible. Thanks Obama.

1

u/LadyGreyIcedTea 27d ago

When I started in the working world after college (2007), I paid $35 every other week for a BCBS plan that had no deductible and only like $25 co-pays for specialists.

I remember how bent out of shape I was when they added a $100 co-pay for MRIs in 2010. Now I would kill for that plan.

1

u/Turbulent-Pay1150 24d ago

That’s actually pretty fair based on health cost inflation. If Obamacare held the cost that low yay.

1

1

1

u/PlaneCat3427 27d ago edited 27d ago

I would try Healthcare.gov first. Since you're changing jobs/unemployed you can sign up to see what they can offer you. They may still cover you & cover your premium, if your work's insurance options aren't seen as affordable/meeting minimum value standards. Last year I pulled under 45k self-employed and they still covered a good portion (Around $350/mo) of my monthly premium for a marketplace plan.

That Vitality app thing being used to gauge your health insurance premium has to be one of the worst things I have ever fucking heard of.

1

1

1

u/VelvetElvis 27d ago

Is this an employer self-pay plan? If so, your employer is paying health care costs directly and United is just managing it.

We're on my wife's UHC plan that uses vitality. This far into the year, they probably prorate this year and next year so you don't have earn a year's worth of points in in a couple months. All points earned in 2025 count towards 2026's premiums. They aren't going to dump you right into the most expensive tier. Getting to Bronze and Silver is easy. Gold is annoying but you'll be able to get there and it's worth it. People who get Platinum are masochists.

A lot of things you should be doing anyway count towards points: Flu and Covid boosters, annual dental cleaning, preventative care like colonoscopies, mammograms and pap smears, annual physical, cholesterol and A1C screaming, etc.

If go the the gym regularly or work out independently, get a smart watch and synch it to vitality. It will automatically record your workouts and you're there.

There's a whole lot of stuff that counts.

Our RX coverage is through Caremark, not United so prescription copays aren't included in either the deductible or OOP limit. It is covered in the premiums, at least. Ask about that. You'll probably be dealing with Caremark, Optum Rx, or something else like that.

We have the equivalent of Signature Gold. If you have any kind of chronic condition, that's really the one you want, assuming it's PPO the others are HMOs. Since the chart is the same in her benefits guide as what you have here, down to the font and colors, I suspect that's the case.

The details of what's covered are going to differ between employers and and states.

1

u/bugaloo2u2 27d ago

Not sure why ur complaining. I pay an $800/monthly premium for a bronze plan with a $7,500 annual deductible. Yeah.

1

u/UpsetAfternoon3243 27d ago

Man I’m reading this thinking these are awesome rates for healthcare. You should see what my company offers. I pay $1400/month for myself and two daughters and I have a $7500 deductible with a lot of things not covered.

1

1

u/TheWordBaker 27d ago

My experience with Vitality was that new hires were given the full discount until the employee had a complete year to earn a discounted premium that is then applied the following year. So the points I earn through 2025 determines the total discount applied to 2026.

1

u/oklutz 26d ago

This is my issue with HDHPs/HSAs. I wouldn’t mind so much if they were an alternative plan offered in addition to the standard PPO and HMO options already available. But they’ve been supplanting low deductible/flat copay plans for quite a while.

I’m not sure why an employer has to offer two HDHP plans when they only offer one standard plan. In a given year most people don’t reach the deductible so it’s not like there’s some remarkable difference in benefits.

Benefits on non-HDHP have gotten progressively worse while employers do everything they can to incentivize employees to choose an HDHP with an HSA. When they make benefits worse and hike up premiums on standard plans, and then offer “free” plan where they contribute to an HSA, of course that’s attractive.

Also: The tier program you mentioned seems to be a replacement for them losing the ability to charge more for “pre-existing conditions”, honestly. Health incentive programs should come in the form of a check in the mail, even if it’s a reimbursement check for a thing I’ve already bought. To come in the form of a lowered premium feels pretty dystopian to me.

1

u/thesillymachine 26d ago

Go with the value HSA. The money you put in can actually be used for expenses. Not just at the doctor, but dentist, eye, chiropractor, and even bandaids.

1

u/whiskeyandprozac 24d ago

I'm sorry your rates are going up, but if it makes you feel any better I pay $1000 a month as a single person. I would kill for these prices.

1

u/QuantumDwarf 22d ago

I just want to point out this isn’t a United vs Aetna thing. Your company decides completely your deductible and the amount you pay for your portion of your premium. Your new employer is paying less of the premiums. So depending how much $$ you make in base pay it may be a pay cut.

1

u/VanillaBeaner1 20d ago

Absolutely look up your medications/doses on Good RX (this will be your cost and insurance wont be used) Often you can get your prescription for less out of pocket without going through insurance (you cant do both for same prescription) Call your audiology services and request self pay estimates in writing for the type of service you use(look at your bill or "EOB" to see the CPT code they use for the charges. Everybody needs catastrophic coverage-car crash, broken bones, hospitalization etc, look a 'MAX OUT OF POCKET". Ask your PCP office how much out of pocket appt costs you. (Look back at your current insurance EOBS for CPT codes for the labs that get ordered annually and see those prices). If surgery is likely again2026, you will need higher insurance coverage. IF your medicines are for stable medical condition or people that are vry healthy and not taking any medications , the high deductible with HCSA and lowest payroll premiums is great plan. The HCSA is triple tax advantaged! Plan would be to have MAX allowable contribution from your checks, PRE-tax into HCSA, (that can make the taxes taken from each check lower as well as your end of year taxes) Even better is to try to pay out of pocket the healthcare bills/prescriptions rather than take from the HCSA. Funds taken from HCSA to pay healthcare costs are TAX FREE. This is an account you can amass a LOT of money in over time and be an addition to your retirement funds! You would definitely want to contribute enough to cover maximum out of pocket deductibles, IN CASE God forbid you had catastrophic medical event. ALWAYS contact the Medical office/hospital/doctors billing number and ask for assistance. (Many will lower the bill if yu will pay cash now) Most HCSA will allow you to invest some of your funds after a certain balance is there. Anyone that can use the high deductible HCSA with low premiums should go for it, and put the extra money you would be throwing away for insurance premiums,directly into HCSA that is YOURS even when you leave the job. Take advantage of any gimmicks to get extra dollars from employer. ALWAYS put enough in their 401K to get whatever % employer will match if that is available. And finally, every time you get a % raise, increase your 401K contribution by that %. You won;t miss money you havent had, and you will build retirement funds compounding over time. ALWAYS pay your savings as a monthly bill, even if that means assigning $10/month as your "savings bill".

1

u/Unlucky-Work3678 28d ago

The price of HSA is typical, actually better than mine.

When you think it's expensive, remember that your employer probably pays 90% of it, you only pay 10% or maybe 15%.

It's what it is. Medical/medical cost is the same to any person no matter they make 50k or 5 million. (I know it's off topic but that's why living in expensive state can make more sense only because of this)

•

u/AutoModerator 28d ago

Thank you for your submission, /u/quinndoline. Please read the following carefully to avoid post removal:

If there is a medical emergency, please call 911 or go to your nearest hospital.

Questions about what plan to choose? Please read through this post to understand your choices.

If you haven't provided this information already, please edit your post to include your age, state, and estimated gross (pre-tax) income to help the community better serve you.

If you have an EOB (explanation of benefits) available from your insurance website, have it handy as many answers can depend on what your insurance EOB states.

Some common questions and answers can be found here.

Reminder that solicitation/spamming is grounds for a permanent ban. Please report solicitation to the Mod team and let us know if you receive solicitation via PM.

Be kind to one another!

I am a bot, and this action was performed automatically. Please contact the moderators of this subreddit if you have any questions or concerns.