r/debtfree • u/IncompletePieces • 8d ago

Is National Debt Relief a good option?

{kind=link}

I know this debt amount isn't a lot for many, but seeing as I was out of work for roughly 3 months due to a sustained injury (with no insurance or backpay or being able to claim disability) my debt has grown since, and it has become a little overwhelming for me to be able pay back this + other debt I have...would accepting the National Debt Relief be a good option for me? (creditors are syncbank, discover, and capital)

3

u/attachedtothreads 7d ago

u/SavageLife6 made a good point about calling up your credit card companies to ask for a hardship program where they lower your interest rate in exchange for freezing or closing your accounts.

While there's a dip in your credit score, it's much less harmful than debt relief. With the latter, it may count as income of there's any forgiven debt.

If the credit cards won't give you the hardship, then call the non-profit debt management program the National Foundation for Credit Counseling for help. They negotiate on your behalf to lower the interest rate in exchange for closing your accounts. There's a small monthly fee of $5-$10/account you enroll with them and a one-time setup fee of $50-$75. Again, your credit score takes a hit, but not nearly as bad as with debt relief.

Here's more on the difference between the two: https://www.consumerfinance.gov/ask-cfpb/what-is-the-difference-between-credit-counseling-and-debt-settlement-debt-consolidation-or-credit-repair-en-1449/

3

u/wagerdude 8d ago

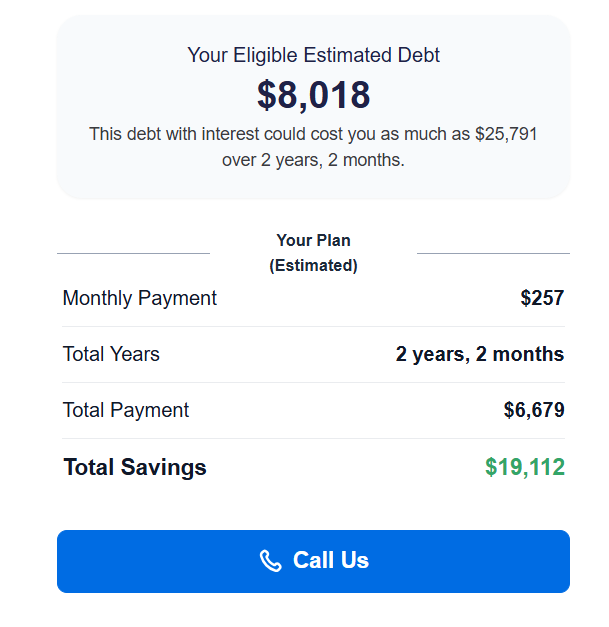

For this amount? I mean, $8k isn’t a lot to pay off, especially if it’s in smaller parts. But if you’re struggling, it’s not a bad idea at all, you pay $257 and you could easily atleast double that with some work and pay it off much quicker.

If you’re thinking of paying it off the way you’ve been doing, snowballing might be for you

Best wishes.

2

u/IncompletePieces 8d ago

my total debt is around 12k, but this was the only debt that was eligible for the relief program. Work hours have been hard on me right now, especially since they were cut back due to my injury.

I was mostly curious as I read a post that said it wasn't the best option as I could eventually end up paying more in fees

2

u/wagerdude 8d ago

Wife made a 20 something K debt relief. Went okayish for her. It’s not a terrible option but it all comes down to your financing.. 12k can be paid off relatively easy, but if your work hours are getting cut etc but you’re healthy overall, doordashing isn’t a terrible, terrible way of making some money. Essentially it’s doordash lending you money lol that you return in gas but it can help temporarily.

Look into where does your money go every month, recalculate what is a must expense and what is a want expense, then snowball it if you need quick mental relief.

I promise you, it’s not that bad at all! You’re doing fine, just a little bump on the road

1

u/nerfsmurf 7d ago

Compare vs outright paying off (hopefully with negotiated amounts) using DefineYourDollars

1

u/mataw95 6d ago

Are you prepared to stop making payments, deal with collection calls, and even risk lawsuits? That’s what debt settlement companies require. They can work, but they’re really for people who are already way behind and have no other options. With $12K of debt, you might not need to go down that road. First step is to call your creditors directly and ask for a hardship program. Sometimes they’ll lower the rate or set up a temporary reduced payment. If that doesn’t give you enough breathing room, a nonprofit credit counseling program could consolidate your cards into one payment with lower interest.

7

u/SavageLife6 8d ago

I don't have experience personally but what I've heard from others is the "debt relief" is really just preying on folks that wanna do the right thing.

Call your debtors and come up with a payment arrangement maybe a lower APR for a bit anything you can get. Paying more money for "help" on top of the situation is not going to be better.

If you find a lower loan rate thats worth looking into or a 0 APR balance transfer. Thats really it though.